The liberalisation was till 31st December and has not been extended

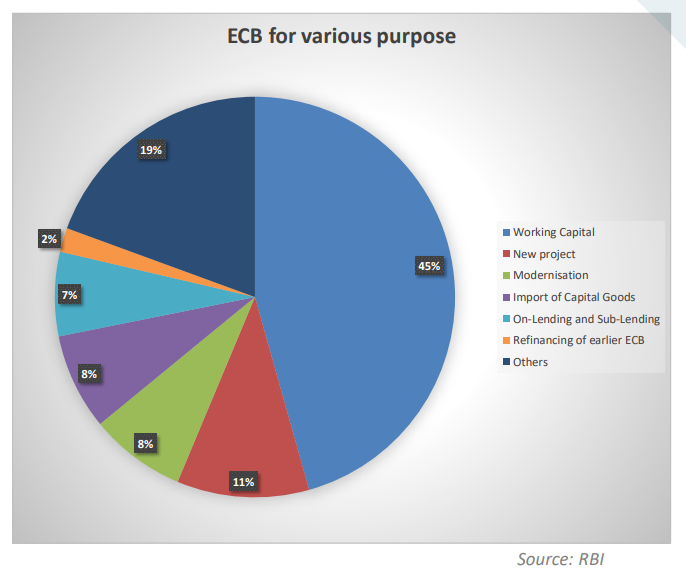

External Commercial Borrowings for Various Purpose

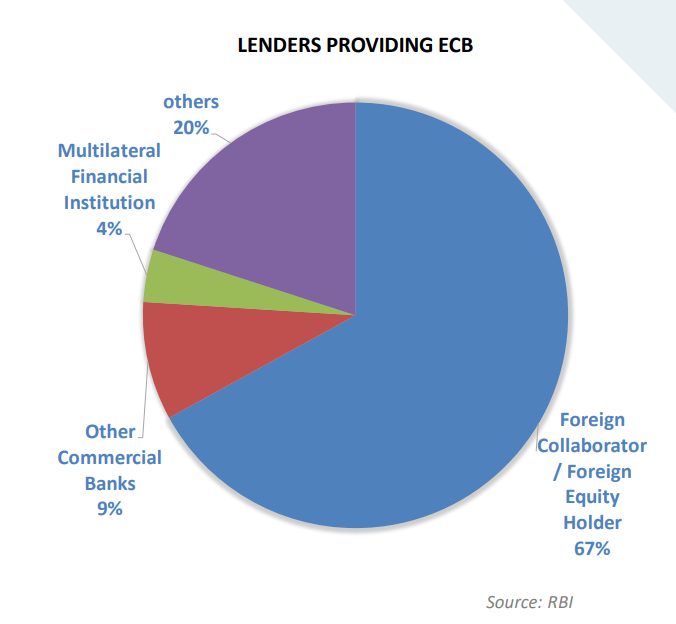

Lenders Providing ECB to Indian Entity

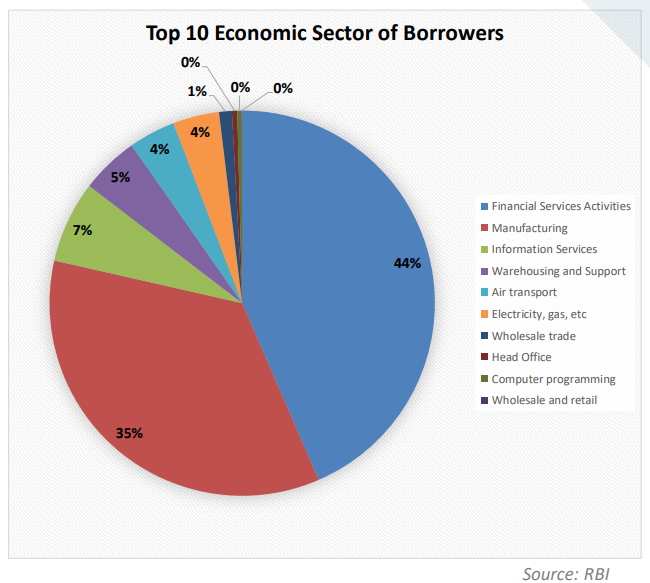

Economic Sectors of Borrowers

Note: RBI FAQ Qn 5 – LLPs are not eligible borroweras not eligible to receive FDI (LLP eligible to receive Foreign Investment under FEMA NDI [earlier FEMA 20(R)]

The lender should be resident of FATF or IOSCO compliant country, including on transfer of ECB. However,

FATF: A country that is a member of Financial Action Task Force (FATF)

IOSCO: A country whose securities market regulator is a signatory to the International Organization of Securities Commission’s (IOSCO’s)

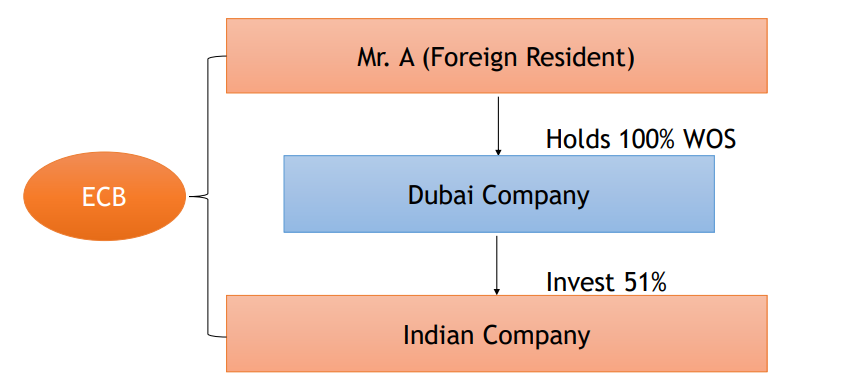

Is Mr A permitted to provide ECB directly to the Indian Co.?

ECB proceeds cannot be utilised for-

a) Real estate activities

b) Investment in capital market

c) Equity investment. (domestic)

d) Working capital purposes except from foreign equity holder.

e) General corporate purposes except from foreign equity holder.

f) Repayment of Rupee loans except from foreign equity holder.

g) On-lending to entities for the above activities, except in case of ECB raised by NBFCs

Note: RBI FAQs No. 23 – The reimbursement of expenditure incurred in the past is not a permissible end-use under the ECB framework

Note: RBI FAQs No. 26 – Refinancing of INR ECB with FCY ECB is not permitted

MAMP for ECB will be 3 years. Call and put options, if any, shall not be exercisable prior to completion of minimum average maturity.

| Sr. No. | Raised by | Raised upto/for | MAMP |

| (a) | Manufacturing Companies | Upto USD 50 million or its equivalent per FY | 1 Year |

| (b) | Foreign equity holder | a. Working capital purposes or general corporate purposes |

Note: RBI FAQs No. 14 – Repayment of principal of ECB can start before the completion of MAMP

Calculation of Average Maturity- An Illustration ABC LTD. Loan Amount = USD 2 million

| Date of drawal/repayment | Drawal | Repayment | Balance | No. of Days** balance with the borrower | Product= (Col.4 * Col. 5)/(Loan amount * 360) |

| Col. 1 | Col. 2 | Col. 3 | Col. 4 | Col. 5 | Col. 6 |

| 05/11/2007 | 0.75 | 0.75 | 24 | 0.0250 | |

| 06/05/2007 | 0.50 | 1.25 | 85 | 0.1476 | |

| 08/31/2007 | 0.75 | 2.00 | 477 | 1.3250 | |

| 12/27/2008 | 0.20 | 1.80 | 180 | 0.4500 | |

| 06/27/2009 | 0.25 | 1.55 | 180 | 0.3875 | |

| 12/27/2009 | 0.25 | 1.30 | 180 | 0.3250 | |

| 06/27/2010 | 0.30 | 1.00 | 180 | 0.2500 | |

| 12/27/2010 | 0.25 | 0.75 | 180 | 0.1875 | |

| 06/27/2011 | 0.25 | 0.50 | 180 | 0.1250 | |

| 12/27/2011 | 0.25 | 0.25 | 180 | 0.0625 | |

| 06/27/2012 | 0.25 | 0.00 |

Average Maturity= 3.2851 **

Calculated by = DAYS360 (firstdate, seconddate, 360)

FCY ECB

INR ECB

Others

Note: RBI FAQs No. 21 – All-in-cost should be within the applicable ceiling at all times, e.g., breach of all-in-cost ceiling in the first year and a much lower all-in-cost in the second year so as to comply on an average, is not permitted.

ECB Amount

Includes all outstanding amount of all ECBs (other than INR denominated) and The proposed one (only outstanding ECB amounts in case of refinancing)

Equity

Includes the paid-up capital and free reserves (including the share premium received in foreign currency) as per the latest audited balance sheet.

ECB and Equity

Amounts will be calculated with respect to the foreign equity holder.

More Than One Foreign Equity Holders

In the borrowing company – the portion of the share premium in foreign currency brought in by the lender(s) concerned shall only be considered for calculating the ratio

Note: RBI FAQs No. 18 – Any debit balance in the profit and loss account as per the latest audited balance sheet of the Eligible Borrower should be deducted from the equity

Form ECB: Borrower is required to submit Form ECB in duplicate with AD Bank. AD Bank will forward one copy to the Director, Balance of payments statistics division, Department of Statistics and Information Management, RBI

Loan Registration Number (LRN)

Changes in terms and conditions of ECB

Monthly Reporting of actual transactions

Delay in reporting of drawdown of ECB proceeds before obtaining LRN or delay in submission of Form ECB 2 returns can be regularized by payment of LSF as under:

| Sr. No. | Reporting Delays | LSF Amount (INR) |

| 1. | Form ECB, Form ECB-2, Revised Form ECB | [7500 + (0.025% * A*n)] |

‘A’ = Amount involved in the delayed reporting.

‘A’ = for any ECB-2 return will be the gross inflow or outflow (including interest and other charges), whichever is more ‘n’ = number of years of delay in submission rounded upward to the nearest month (up to 2 Decimal).

Note: RBI FAQs No. 39 & 40 – The facility for opting for LSF shall be available up to three years from the due date of reporting/submission. Also, LSF is applicable for non-submission of each Form ECB 2, including Nil returns

Permitted subject to:

Eligibility

Recognised Lender

Amount, Average Maturity & All-in-costs

Form and End-use

Currency and conversion

Security and Guarantee

Others

TC refer to credits extended directly by the overseas supplier, bank, financial institutions and other permitted recognised lenders for imports of capital/non-capital goods.

| Sr. No. | Parameters | FCY denominated TC | INR denominated TC |

| (a) | Forms of TC | Buyers’ Credit and Suppliers’ Credit | |

| (b) | Eligible borrower | Person resident in India acting as an importer | |

| (c) | Amount under automatic route | a. Up to USD 150 million or equivalent per import transaction for oil/gas refining & marketing, airline and shipping companies | |

b. For non-capital goods, this period shall be up to 1 year or the operating cycle whichever is less.

Trade Credits scheme for SEZ/FTWZ/DTA

FAQ

An Indian Shipping Company purchased a ship on suppliers credit of 3 The Company was not able to repay the suppliers credit within 3 years. Can the Company apply for an extension of the trade credit for 2 years?

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content: